The global Wearable Medical Devices Market is projected to grow from an estimated USD 31.4 billion in 2025 to approximately USD 80.5–83.2 billion by 2035, exhibiting a CAGR of ~9.5–10.5% during the forecast period. Rising prevalence of chronic diseases, increasing demand for remote patient monitoring, integration of advanced sensors and AI, and growing adoption of fitness and health monitoring devices are key growth factors. Wearable medical devices — including smartwatches, biosensors, wearable ECG monitors, glucose monitors, and body-worn patches — are transforming healthcare delivery by enabling continuous health tracking, early diagnosis, and personalized treatment.

Market growth is further supported by favorable reimbursement policies, rising healthcare IT infrastructure investments, and an aging global population seeking non-invasive monitoring solutions.

Key Drivers in Wearable Medical Devices Market:

- Rise of Chronic Diseases: Increasing cases of diabetes, cardiovascular disorders, hypertension, and respiratory illnesses drive demand for continuous monitoring and preventive care.

- Healthcare Digitization & Telehealth Growth: Expanded telemedicine services and remote patient management models fuel adoption of wearable medical devices.

- Technological Advancements: Integration of AI, IoT, cloud platforms, advanced biosensors, and predictive algorithms enhances device capabilities and user experience.

- Consumer Awareness: Rising health consciousness and emphasis on data-driven wellness support widespread use of wearable medical devices.

- Favourable Reimbursement Policies: Supportive government initiatives and insurance reimbursements for remote monitoring devices encourage market growth.

Key Restraints Drivers in Wearable Medical Devices Market:

- Data Privacy & Security Concerns: Collection and transmission of sensitive health data through wearable devices raises cybersecurity and privacy issues.

- Regulatory & Compliance Challenges: Strict regulatory approvals and certification requirements can delay product launches.

- Battery & Power Limitations: Continuous operation of sensors and connectivity modules increases power demand; limited battery life can deter usage.

- High Cost of Advanced Devices: Premium pricing of high-end wearable medical devices may restrict adoption, particularly in price-sensitive markets.

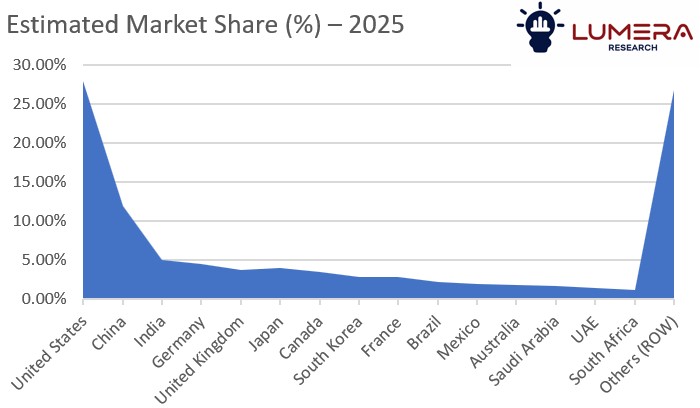

Regional Dynamics:

- North America represents the largest market, supported by advanced healthcare infrastructure, strong adoption of digital health technologies, high healthcare spending, and supportive reimbursement frameworks.

- Europe shows steady growth driven by increasing adoption of connected healthcare devices, government initiatives promoting preventive care, and integration of wearable devices in chronic disease management programs.

- Asia Pacific is the fastest-growing region, propelled by rising healthcare awareness, expanding middle-class population, growing prevalence of lifestyle diseases, and increasing investments in telehealth infrastructure.

- Latin America exhibits growing demand with expanding healthcare access and digital health adoption in countries like Brazil and Mexico.

- Middle East & Africa shows gradual growth due to rising healthcare digitization, increased healthcare IT spending, and telemedicine deployment.

Quick Market Figures:

- 2025 Market Size: USD ~31.4 Billion

- 2035 Market Size (Projected): USD ~80.5–83.2 Billion

- CAGR (2025–2035): ~9.5–10.5%

- Leading Regional Growth: Asia Pacific (fastest-growing)

Key Players in the Wearable Medical Devices Market:

- Apple Inc.

- Fitbit (Google LLC)

- Garmin Ltd.

- Medtronic plc

- Abbott Laboratories

- Philips Healthcare

- Samsung Electronics

- Huawei Technologies

- BioTelemetry (Philips)

- Dexcom, Inc.

- Omron Healthcare

- Withings SA

- iRhythm Technologies

- Fitbit Health Solutions

- Xiaomi Corporation

- Koninklijke Philips N.V.

- Masimo Corporation

- Zephyr Technology

- Valencell, Inc.

- AliveCor, Inc.

- Proteus Digital Health

- Biobeat Technologies

- Qardio, Inc.

- ResMed Inc.

- Honeywell International Inc.