Polyisocyanurate Insulation Market value is USD 14.2 billion in 2024, projected to reach between USD 24.3–25.6 billion by 2033–2035 (CAGR approximately 6.1–6.6%). The global polyisocyanurate insulation market is growing steadily as demand for energy-efficient, fire-resistant building materials rises in residential, commercial, and industrial segments. Stringent building codes, green construction trends, and technological innovations are fueling expansion.

Leading segments in Polyisocyanurate Insulation:

Rigid foam board products dominate, accounting for approximately 80% of the market share due to their versatility and performance in thermal applications.

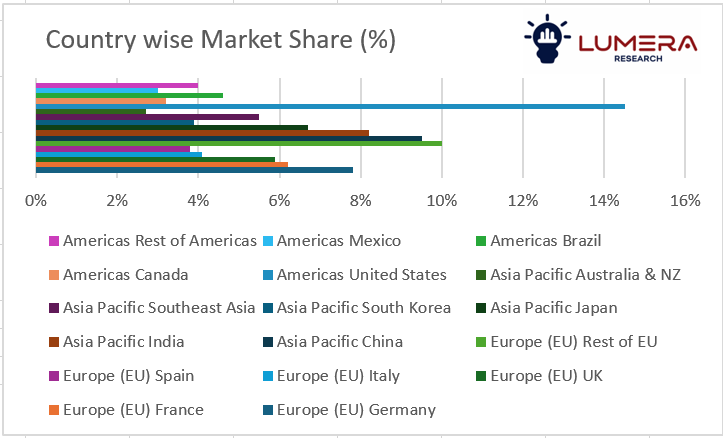

Thermal insulation remains the leading application (over 70% share), with wide adoption in roofing, wall insulation, and cold storage facilities. Asia-Pacific is the fastest-growing region—driven by construction growth in China, India, and Southeast Asia—while North America maintains the largest share due to mature infrastructure and stringent energy codes.

Drivers:

- Regulatory ramp-up on energy efficiency and green building standards bolsters demand for high-R-value insulation.

- Urbanization and construction booms in developing economies accelerate the uptake of polyiso solutions.

- Technological advances—such as prefabricated panels, enhanced fire retardancy, and moisture-resistant core formulations—expand application versatility.

- Market shift toward sustainable and resilient building materials increases preference for polyisocyanurate’s durability and eco-performance.

Restraints:

- Price volatility and rising cost of raw polyol and isocyanurate materials can compress margins or slow adoption.

- Complexity in manufacturing multilayer or laminated solutions raises capital and operational requirements.

- Recycling or disposal of multilayer and coated insulated boards remains a sustainability challenge.

- Limited awareness or traditional preferences in some regions can delay adoption of newer insulation technologies.

Polyisocyanurate Insulation Market Regional Dynamics:

North America: Largest market in value, driven by strict energy codes, retrofit demand, and established construction frameworks.

Europe: Steady growth underpinned by sustainable building mandates, fire safety regulations, and modernization of commercial and industrial stock.

Asia-Pacific: Fastest-growing region, propelled by rapid urban construction, infrastructure investment, and climate resilience priorities.

Quick Market Figures:

- 2024 market size: USD 14.2 Billion

- 2033–2035 market size (projected): USD 24.3–25.6 Billion

- CAGR (2024–2033/35): ~6.1–6.6%

- Leading product type (2024): Rigid foam board (~80% share)

- Leading application (2024): Thermal insulation (~73% share)

- Regional leader: North America (highest value), Asia-Pacific (fastest growing region)

Key Players in Polyisocyanurate Insulation Market:

- BASF

- DowDuPont

- Owens Corning

- Saint-Gobain

- Kingspan Group

- Honeywell International

- Johns Manville

- Sika AG

- Stepan Company

- IKO Industries

- Knauf Insulation

- Atlas Roofing Corporation

- GAF Materials Corporation

- Carlisle SynTec

- Hunter Panels

- Covestro

- Chemours

- Nippon Shokubai

- Recticel