Overview:

The fortified pet food market was valued at approximately USD 10.1 billion in 2024. Reflecting the increasing focus on pet health and overall well-being by their owners, the market is projected to reach USD 10.7 billion by the end of 2025. Industry experts anticipate continued robust growth, with a projected compound annual growth rate (CAGR) of 5.7% from 2025 to 2035, driving the market size to an estimated USD 18.8 billion by 2035.

The expansion of the pet food fortification sector is significantly influenced by the trend of pet humanization. This phenomenon leads pet owners to invest more readily in highly nutritious products that are perceived to contribute to their pets’ comprehensive health.

Food items enriched with essential vitamins, necessary minerals, amino acids, and beneficial antioxidants are experiencing escalating demand. Consumers increasingly associate these added ingredients with notable health improvements in their pets, such as enhanced immune system function, stronger musculoskeletal structures, improved coat health, and higher energy levels. Several prominent manufacturers have developed specialized nutritional formulations targeting specific breed requirements and various life stage conditions.

The broadened access to and increased interaction with veterinary healthcare professionals have significantly impacted consumer purchasing patterns. Pet owners now possess greater knowledge and actively seek food solutions that deliver specific functional advantages, including support for joint health, digestive function, or skin condition. Manufacturers are responding by introducing product lines tailored to these needs, such as puppy food with added calcium or senior diets supplemented with chondroitin and glucosamine.

Furthermore, digital platforms have played a crucial role in expanding product accessibility and disseminating vital information, including consumer feedback and product ratings. Distribution capabilities have improved substantially through enhanced product availability via online channels and specialized pet retail outlets, effectively meeting the rising demand. The growing preference for clean-label and organic options, particularly among urban consumers with environmental awareness, is also positively contributing to category growth.

The sector’s trajectory over the next decade will continue to be supported by the ongoing launch of a wider variety of products, increasing functional specialization in formulations, and the reliance on scientific evidence to back ingredient-based claims. These factors are expected to reshape the competitive environment within the foreseeable future.

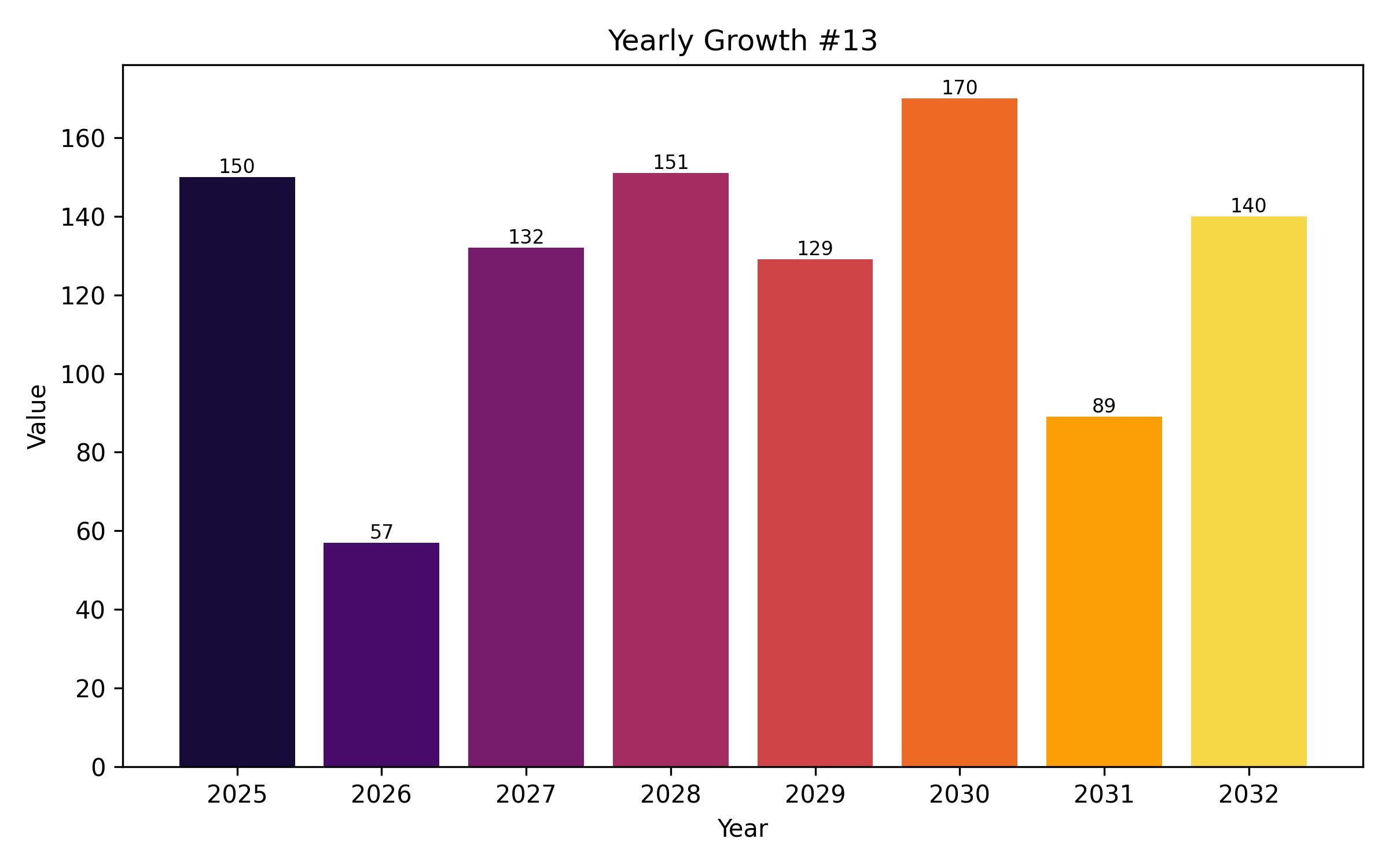

A comparison of the projected compound annual growth rates (CAGR) between the initial period (starting 2024) and the current forecast period (starting 2025) for the global fortified pet food market offers valuable insights into evolving revenue trends. This comparative analysis helps stakeholders understand the market’s performance shifts and anticipated direction within the year. The analysis uses a semi-annual approach, defining H1 as January to June and H2 as July to December.

For the first half (H1) of the 2024 to 2034 period, the market is expected to exhibit a CAGR of 5.4%, while the second half (H2) is anticipated to show a slightly higher growth rate of 5.7%. Looking ahead, for the H1 of the 2025 to 2035 period, the CAGR is projected to be stable at 5.8%. By H2 2035, the market growth rate is expected to reach around 6.0%, reflecting a sustained upward trend. The market demonstrated an increase of 40 basis points in growth during H1 year-over-year and 30 basis points in H2.

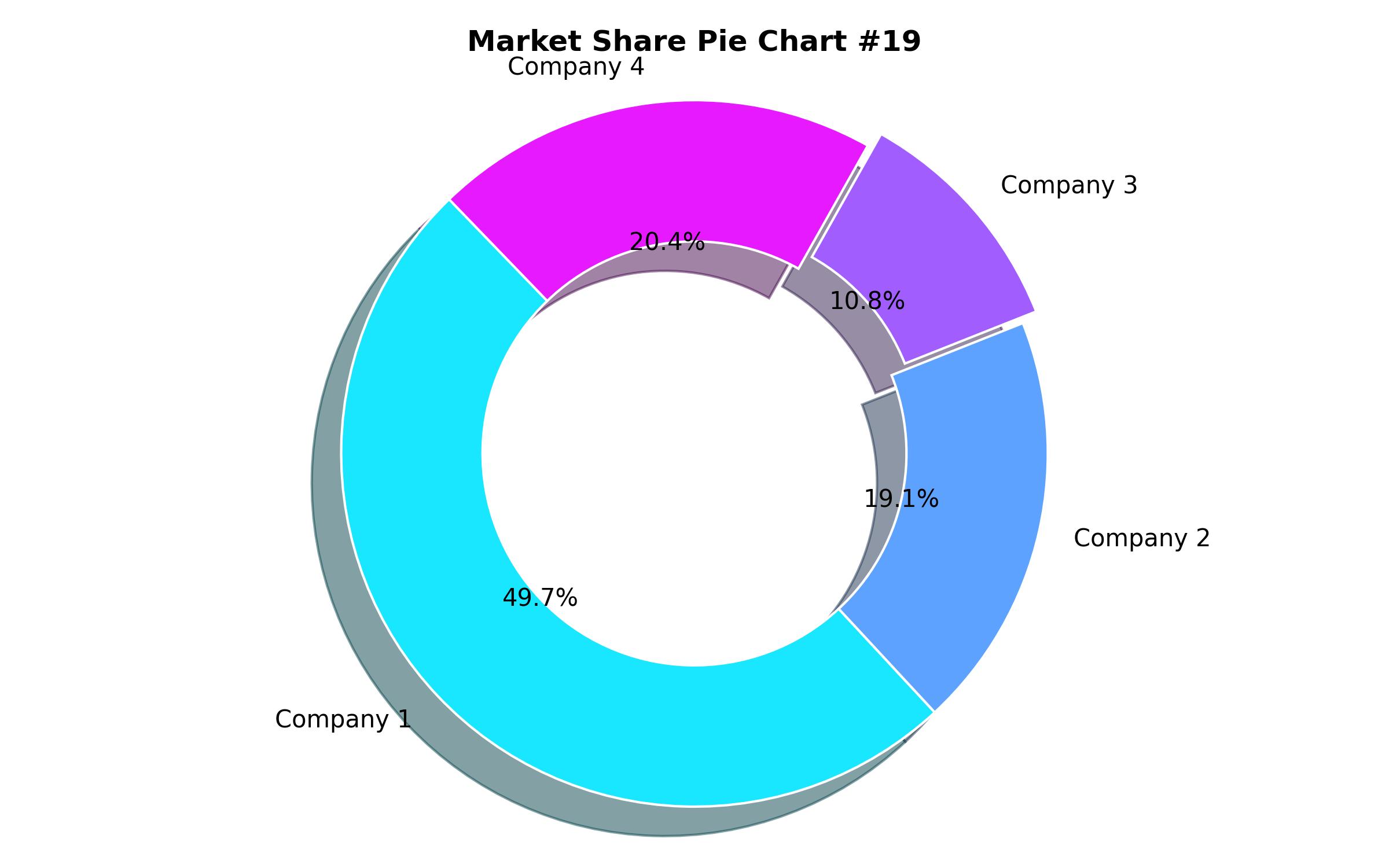

The competitive landscape is stratified into distinct tiers. Tier 1 consists of globally recognized leaders with extensive brand equity, robust distribution networks, and substantial investment in research and development. These companies have cultivated consumer trust over decades through scientific innovation and strategic market presence. An example is Nestlé Purina PetCare, offering nutrient-dense products across various price points, including their Pro Plan line enriched with vitamins, minerals, and probiotics, utilizing cutting-edge nutritional science and global supply chains.

Mars Petcare also holds a prominent position in Tier 1, particularly with premium fortified brands such as Royal Canin and Eukanuba, which address specific health needs like managing weight, supporting joints, and improving gastrointestinal health. They invest heavily in partnerships with veterinary professionals and focus on sustainability initiatives and personalized nutritional solutions, leveraging their significant market influence.

Tier 2 comprises brands that possess a strong market presence but typically operate on a smaller scale compared to Tier 1 companies. This group includes Hill’s Pet Nutrition, known for its Science Diet and Prescription Diet lines, which provide clinically formulated, fortified pet foods designed to manage specific health conditions like renal issues or digestive disorders.

Blue Buffalo is another key player in Tier 2, recognized for combining natural ingredients with added vitamins, minerals, and antioxidants in products like their Life Protection Formula. They cater to pet owners seeking specialized, health-oriented formulas. Although their global volume may not match Tier 1, they have strong market penetration, especially in North America and specific global niche areas, establishing themselves as significant competitors in the fortified segment.

Tier 3 includes specialized and emerging businesses introducing fortified pet food products that emphasize organic, holistic, or hypoallergenic attributes. Examples like The Honest Kitchen, Wellness Pet Food, and Open Farm are making strides with clean-label formulations incorporating probiotics, taurine, and omega fatty acids.

These companies often rely on alternative distribution strategies such as direct-to-consumer sales, subscription box services, and independent pet stores. Their ability to innovate by focusing on trends like grain-free options, human-grade ingredients, or plant-based recipes attracts health-conscious consumers who prioritize transparency and ethically sourced components. While smaller in scale, their rapid growth and devoted customer base position them as potential disruptors within the fortified pet food market.

| Report Attribute | Details |

|---|---|

| Market Size in 2025 | USD 10.7 billion |

| Revenue Forecast for 2035 | USD 18.8 billion |

| Growth Rate (CAGR) | 5.7% from 2025 to 2035 |

| Base Year for Estimation | 2024 |

| Historical Data | 2018 – 2023 |

| Forecast Period | 2025 – 2035 |

| Quantitative Units | Revenue in USD million/billion and CAGR from 2025 to 2035 |

| Report Coverage | Revenue forecast, company market share, competitive landscape, growth factors, and trends |

| Covered Segments | Pet Type, Form, Distribution Channel, and Region |

| Regional Scope | North America, Europe, Asia Pacific, Latin America, MEA |

| Country Scope | U.S., Canada, Germany, UK, France, Italy, Spain, China, Japan, India, Brazil, Mexico, South Africa, UAE |

| Key Companies Analyzed | Royal Canin, Nestlé Purina PetCare Company, Mars Inc., Chr. Hansen (Denmark), Koninklijke DSM N.V., DowDuPont, Evonik Industries, Land O’Lakes, Lallemand, Bluestar Adisseo Co., Lesaffre, Alltech, Schouw & Co. |

| Customization Options | Free report customization (up to 8 analysts working days) with purchase. Changes to country, regional, and segment scope |

| Pricing and Purchase Options | Customizable purchase options for tailored research needs |